What The Fed's Action Means

How would I know? I’m an ignoramus on these matters. Here’s what Tom Luongo says—I’m sure he’ll weigh in at more length soon. What follows is to spur thinking:

And now here’s an unroll of Jim Bianco’s thread. Anyone with an opinion, let me know what you think. One thing I’m convinced of—what’s going on with the Fed and Congress and the War is existentially important for America as we have known it:

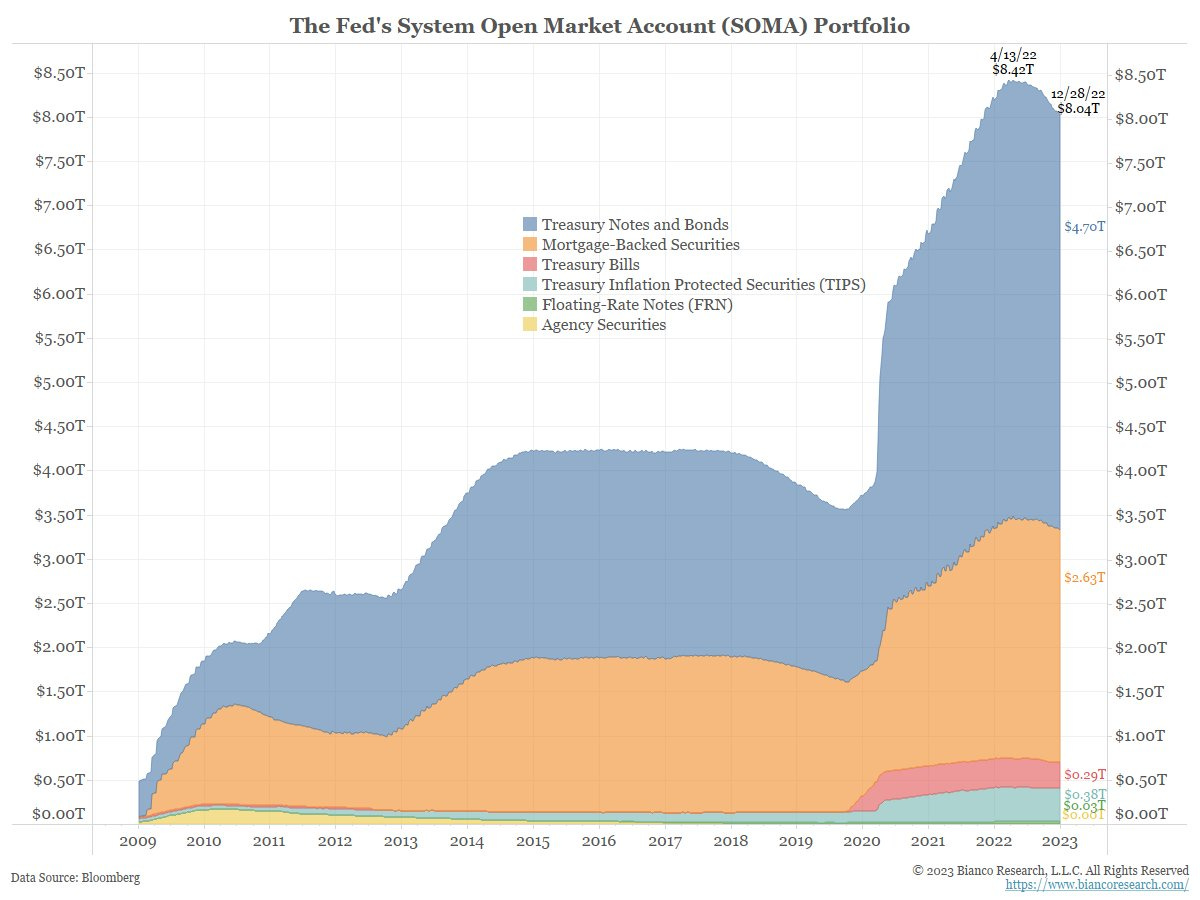

Above this "doom chart" that FinTwit likes to send around.

It is not what you think, the Fed change the accounting making this chart highly misleading.

So, what does it really mean? ...

@LynAldenContact

First ... when the Fed did QE, it bought bonds. When they started QT last spring, they let bonds mature (not sold).

This activity make changes the Fed's balance sheet.

On Dec 28 the Fed balance sheet was $8.55T. Of this, $8.04T was bonds, detailed below.

This $8.04T of bonds all pay a coupon. The Fed uses this income to pay RRP and interest on reserves. What is left over is returned to the the Treasury as a "remittance."

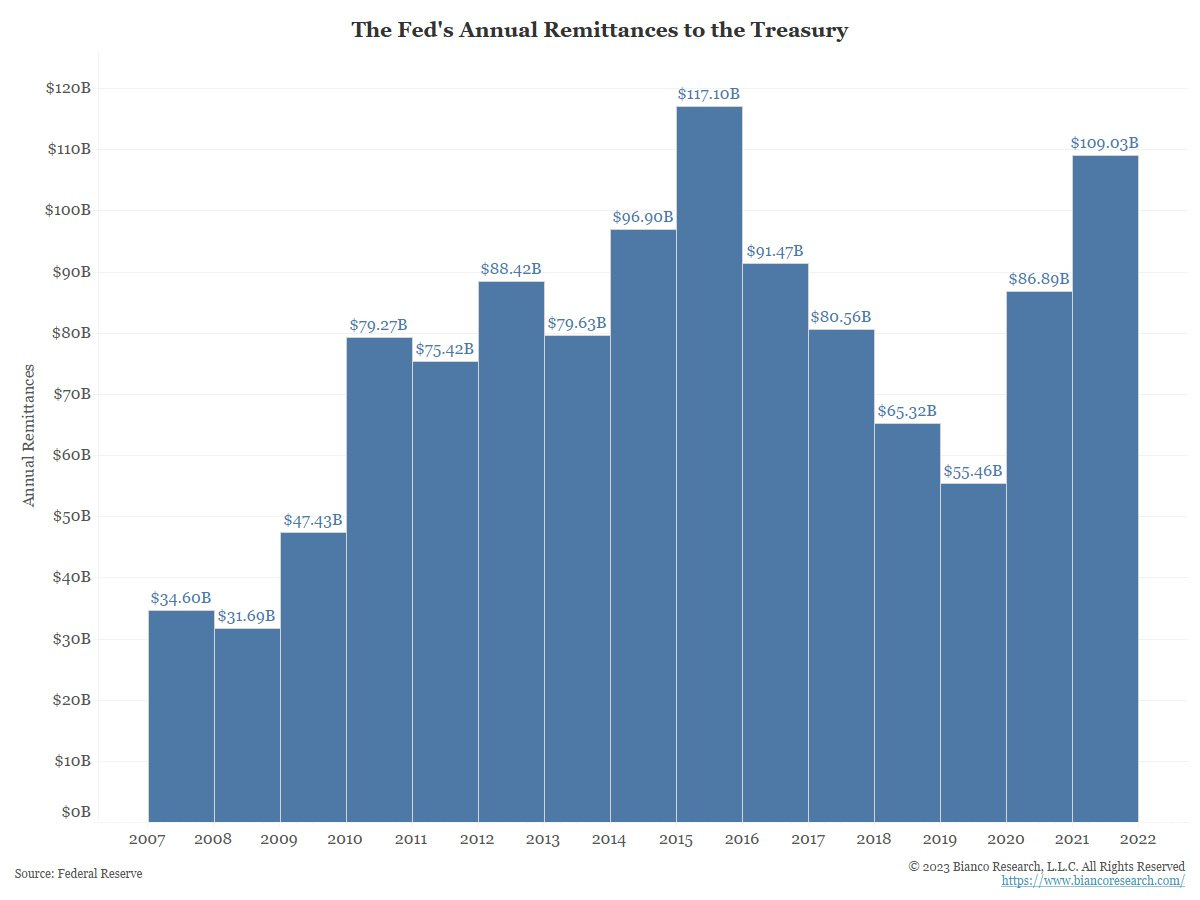

Here is the official amount they have remitted back to Treasury, over $1 trillion since 2011.

By the way, the Fed has an official annual audit done by KPMG.

Here is the 2021 version that includes lots of detail about the remittances, if anyone wants to nerd out on this topic.

federalreserve.gov/aboutthefed/fi…

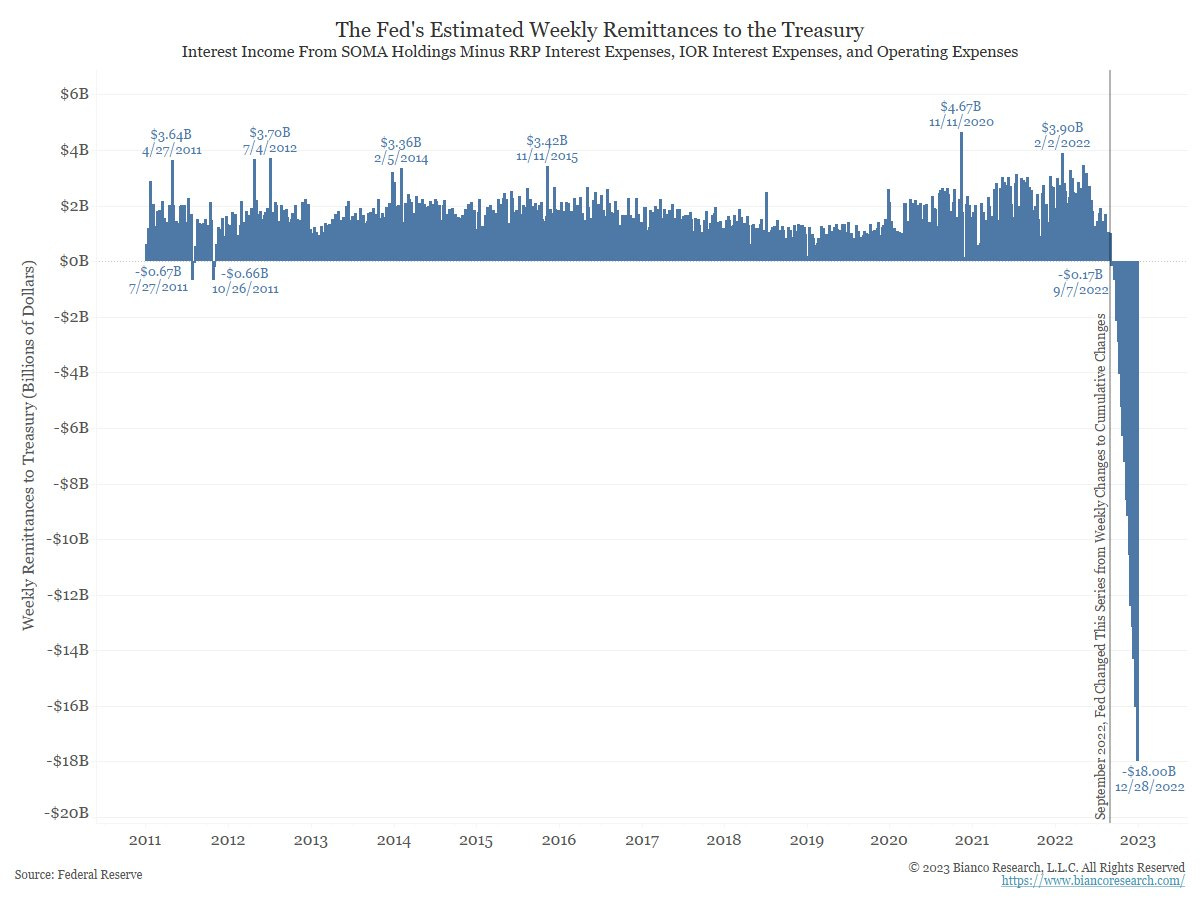

In Sept the Fed changed this series from WEEKLY changes to CUMULATIVE changes. Vertical line.

See table 6, footnote 8

federalreserve.gov/releases/h41/2…

Good explanation why this accounting change makes sense … see the part that starts with “switcharoo.”

wolfstreet.com/2022/12/09/how…

https://federalreserve.gov/releases/h41/20221208/

How Big Are the Fed’s Losses and Where Can We Go See Them? We find a good rubbernecking spot.https://wolfstreet.com/2022/12/09/how-big-are-the-feds-losses-and-where-can-we-go-see-them/

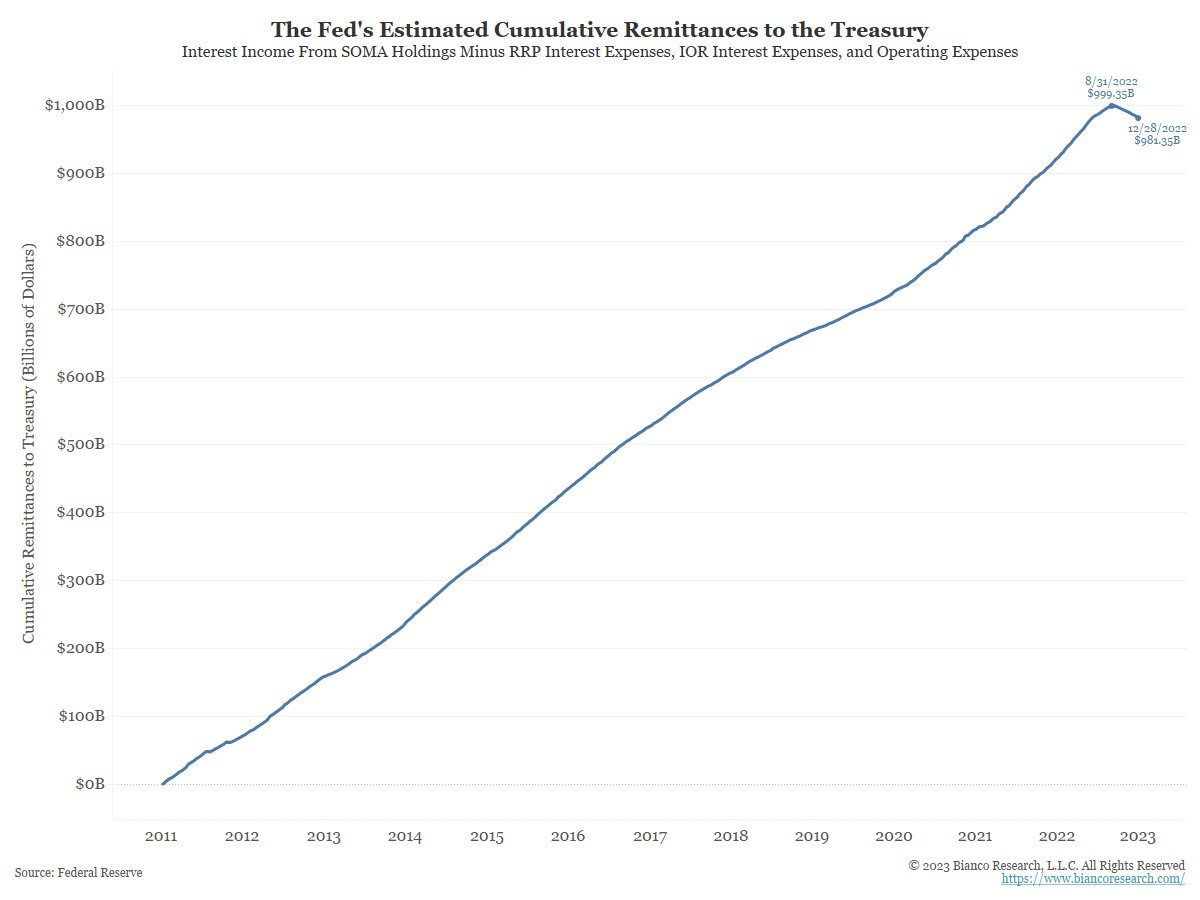

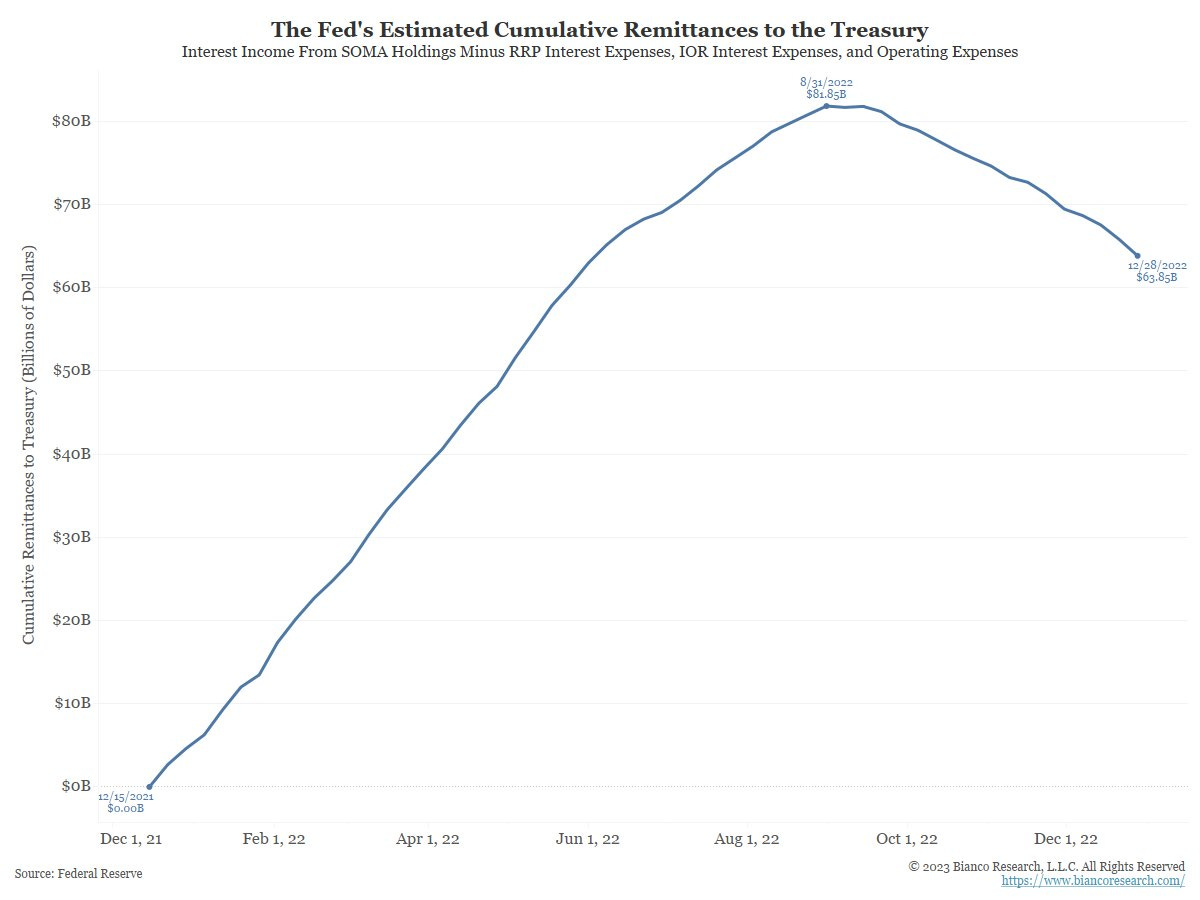

So if I was to rework this chart to all cumulative changes back to 2011, it would look like this.

Now it doesn't look like the end of the financial system anymore.

What about 2022?

Same chart as above but now starts on Jan 1, 2022.

The estimate is about $60B will be remitted to the Treasury in 2022, down from $109B in 2021.

Yes, 2023 their will be no remittances to the Treasury as RRP and Interest on Reserve payments will exceed coupon income. What does it mean?

@judyshel detailed it last summer in the WSJ. Good read on this subject.

Opinion | Why the Fed May Soon Need Treasury Help The central bank will be paying much more in interest on reserves to control inflation.

tl:dr on what happens in 2023.

The Fed will account for these losses by writing an IOU to the Treasury in the form of a ‘deferred asset’.

In English, the Treasury will make these losses back whenever the Fed begins to turn a profit once again.

In the 1930s a brilliant economist, Lord Keynes, came up with deficit spending as the only way to jump-start the economy in a Depression. With prosperity and a booming stock market our deficit should have been erased entirely. Keynes is no longer alive to see how his ideas have been perverted to the point that we run deficits in good times. We who are alive will suffer the consequences.

Follow the money. See if Hunter is cashing in somehow.

Next look at the worst thing that could happen. Note that, and create a list from the worst down to what they are saying what the reason is for their actions. Expect and look for what damage they are attempting while saying the overt reason is.

They're will be something that you will find. Recognize that everything is different and much input is coming from international players, and if the desire is not to make money, then it's to create chaos, damage, publicity and opportunity for foreign players. A good example is the withdrawal from Afghanistan, the end results, the stated results, and the various "mistakes" that were made. Look for similar actions performed via the overt reason for action. Basically it comes down to treachery against the US for foreign interests using our "elected" "leaders"