The Fed Speaks Before The Midterms

It should have been obvious a long time ago that the Fed wants Dem control of Congress to end. Yesterday’s Fed interest rate hike, which is one more hike in a series that are steeper and quicker than ever before, confirms that.

I listened yesterday to an interview with Danielle DiMartino Booth—one which was done before the announced hikes. As usual, Danielle spewed financial and economic data non-stop. The general tenor of her thinking is that, This time is different, but with a twist. What she means by that is, This time there won’t be a Fed bailout. At the same time, she expressed concern that the Fed’s Powell would go too far with the rate increases. She, like everyone else, expected new hikes, but her concern was for where it would all end. In her view, there are signs of significant slowing in the rate of inflation (citing housing prices/costs), and she’d like to see interest rates stop at 6% or a bit lower. She fears that anything else could cause a “systemic event”, one that would lead to an uncontrollable economic crash.

Yesterday afternoon, Jay Powell poured cold water all over hopes for any stop to the interest rate hikes, and indicated that the top level for rates might be increased.

If I may be permitted a criticism of Danielle’s views, it strikes me that she is focused on the Fed—and she is considered an expert reader of the Fed’s tea leaves—solely in the context of the US economy. I say that because all of her gush of stats were drawn from the US—the housing market, auto loans, manufacturing, employment. You name it, she has the stats at her fingertips. However, there is a school of thought that maintains that Powell is fully aware that raising interest rates alone cannot bring price inflation under control if the increases are caused by supply side problems. I’m sure Danielle is well aware of this, but she doesn’t address it directly. But that consideration leads to the question, If Powell understands this, then does that mean that the rate hikes are NOT simply about inflation? Danielle hints that there may be more to this rate hike business, but seems puzzled.

Of course, the guy who has an explanation is Tom Luongo. This morning Luongo and Alex Krainer engaged in a marathon round table discussion with Gonzalo Lira—two and a half hours! I was only able to listen to it off and on. I know that it started with the Fed, moved into Davos v. the Fed, and on to the upcoming midterms here and a lot more.

Regular readers will know that Luongo’s Theory of Everything posits that the major New York commercial banks—which are the shareholders in the Fed—are backing Powell’s struggle with “Davos” globalists (meaning, the old European banking interests and supporters here). Powell is seeking, with apparent success, to reassert US (i.e., Fed) control over US monetary policy. The Fed’s interest rate hikes are part of that struggle in that it drains liquidity from an already bankrupt Europe. In other words, Powell intends to break Europe. In that regard, Luongo—who is obviously a fan of Danielle—starts out by stating that he thinks an interest rate peak of 6%, the figure that Danielle tossed out, should be sufficient to accomplish Powell’s big picture intent of breaking Europe and reasserting control over the US economy and finances.

As you can imagine, over two and a half hours there’s a lot that gets discussed. I did catch one segment in which Luongo and Krainer summarized the Theory of Everything. I should add, that to the credit of Gonzalo Lira, Gonzalo did his best to hold their feet to the fire in terms of justifying the overall theory with specifics. The basic idea as I recall it runs like this.

The protagonists in Europe are the old banking interests—especially Bank of England, City of London, Amsterdam and the Dutch banks, and the French. These interests are allied with the globalist ideologues to form “Davos”, which is the campaign to basically establish one world government—ostensibly through the UN and the IMF, but with Davos pulling the strings. This would include the use of modern tech to establish strict controls over the subject population—economic, financial, political, social. Naturally, the elite wealth in the US has been invited on board as junior partners to the old Euro wealth.

This transformation—the Great Reset—was originally scheduled for completion by 2050, but two Black Swan events intervened. First came Trump, and then the NY commercial banks realized that the whole scheme would mean their subordination to European interests. NY said, No! And began taking concrete steps to decouple from Europe—ditching the linkage via LIBOR for the new US SOFR system.

This turn of events put extreme pressure on Davos, because Europe is basically bankrupt already—head over heels in debt due to socialist policies, and dependent on outside suppliers for energy. This is why Davos had to try to speed up the Great Reset, advancing the target date to 2030. Covid and Election 2020 (the Great Steal) were part of the scheme to remove obstacles for a quicker implementation of the Great Reset. The War on Russia—which Davos wholeheartedly supports—fits in as the move away from carbon based fuel to, as Luongo asserts, a combination of nuclear/hydrogen. In effect, Davos is in a race against the clock. The problem is that for both Russia and the US/Fed, time is on their side but is definitely working against Davos.

What Davos needs to do is to crash the European economy and social system (and you can see this in the US, too, in the form of transgender and other wokeness) and present the subject population with the choice: Debt foregiveness, but we experts run things—surrender your freedom and we’ll take care of you; you’ll own nothing but be happy. But this can’t happen without US cooperation, and the Fed is refusing. Alex Krainer’s brief critique is that the US banks basically have their feet on the ground, and the European globalists (and, of course, their US allies) are living in La-la land. Their Open Society goal is a delusion.

Now, neither Luongo nor Krainer suggest that a defeat of Davos will solve all our problems as a nation, an economy, a society. It’s simply a question of who’s our worst enemy for right now. They maintain that “Davos” is, and I agree. In that regard, I’ll excerpt from an article by Charles Hugh Smith which gets at what may be the root of the problem:

The Era Of All-Powerful Central Banks Is Over

Authored by Charles Hugh Smith via OfTwoMinds blog,

Central bank gaming of Finance is the source of instability.

The era of all-powerful central banks is over for a simple reason: they failed: they failed their citizens, their nations, and they failed the world.

Their policies have pushed wealth and income inequality to extremes that have destabilized the planet's social, political, economic and environmental spheres.

As I have endeavored to explain for many years, this is the only possible outcome of central bank dominance.

Once Finance becomes the primary mover of everything else, then it distorts everything into a skimming machine that benefits the few with access to central bank funding at the expense of everyone else.

Once finance dominates, then both the "market" and government become servants of finance.

I say "markets" because once markets have been financialized, they serve the interests of cartels and monopolies and cease to be markets at all.

Government, regardless of the advertised "brand", becomes an auction where the highest bidder gains control of governance and regulation, which are bent to serve the interests of the few with access to central bank largesse.

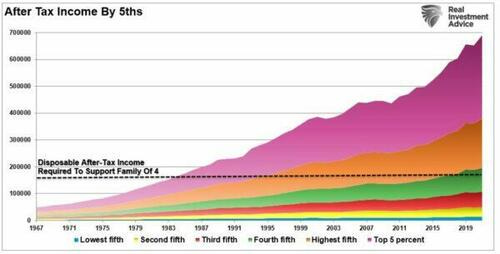

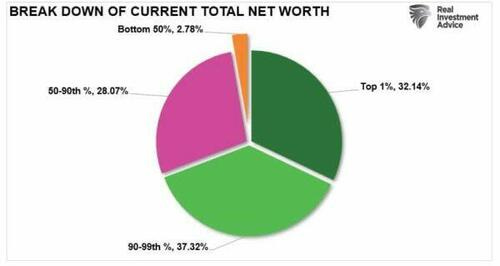

I’m no economist nor am I a financial whiz. How much of this is due to central banks per se, I can’t say. However, I would trace this back to the financialization of the economy, the outsourcing of manufacturing, that began to accelerate in the Reagan years. In that regard Smith provides two charts that are suggestive. There’s a trend at work:

Some would tell you that this is simply the result of a meritocracy, with the talented rising to the top. I think Smith is closer to the truth. Danielle made a telling comment the other day regarding the trillions in Covid handouts. She stated that, as usual, the top and the bottom benefited and the middle got “screwed”. There’s a method to that madness—the middle aren’t usually the troublemakers.

A few days ago Zerohedge also republished an article from Epoch Times. It’s a longish article, but full of graphs and charts drawn from public sources. They all tell the same story—read it and weep:

There are more depressing graphs at the link. I wish fixing things were as easy as holding an election.

Tom Luongo (Give Deflation a Chance!)

@TFL1728

Bingo!

I know this because Powell knows this

Quote Tweet

Santiago Capital

@SantiagoAuFund

The US Government cannot fund itself at 5% forever.

But it can fund itself at 5% for a lot longer than the UK can fund itself at 4.5%, a lot longer than Europe & China can fund themselves at 3%, and a lot longer than Japan can fund itself at 1%.

Let's hope Tom is right. What is certain is that he is spot on about who are enemies are. Who are friends are is harder to tell. Davos will fail but the bodycount will be high.