I would guess that many readers here also follow Sundance at CTH. Those who do will be aware that during the past week Sundance has been particularly focused on the ruling elite that has, in effect, been waging war on the world most of us grew up in. That would be Middle Class America. Sundance and many others see that world being crushed by people who control or influence our public institutions and policies but are either in it for themselves or are crazed ideologues. One way or another, they’re on a power trip the likes of which is arguably unparalleled in human history. What I’d like to attempt in this post is to show the link(s) between domestic and foreign policy—with roots that go back over a century. No, I won’t try to trace those roots that far back. That would be a book.

Thanks for reading Meaning In History! Subscribe for free to receive new posts and support my work.

Now, first of all, a big hat tip to reader Chris who alerted me to the first piece we’ll be looking at. It’s by Ben Hunt. If you’re not familiar with Hunt, you can read his bio here, which will explain why he takes as deep an approach to current issues as he does. I’ve abbreviated this piece to the degree possible, while preserving Hunt’s essential points. It seems to me to present a very lucid summary account of the way our monetary has been run since at least the 60s, and the ramifications not only for our economy but for our political and social way of life. Not that he spells it all out, but I think most readers will see the implications in the context of the hollowing out of our economy—and hollowing out is very much a theme for Hunt.

Now, let me alert you to something else going on here. Hunt is a former academic political scientist, with a focus on America. He tells us up front that the story of the biggest theft in history is, basically, as old as human nature—it’s more a question of degree than a difference in kind. Since this is a story about America, and Hunt sees our constitutional order gravely threatened, this calls into question the very nature of the Great Experiment that the Founding Fathers launched. Has it conclusively failed? Was it always bound to fail? Did it ignore fundamental weaknesses in human nature? Are all largish societies doomed to descend into oligarchy, in spite of the best intentions of the founders?

We are all villagers in Kurtz’s world [he's referring to Józef Korzeniowski'sHeart of Darkness], an unnatural, literally insane world created by proclamation and fiat. Sure, our standard of living may be a little bit better than in the picture above, but the essential hollowness is the same. Maybe worse. And now an implacable agent of change – in the movie it’s the assassin Willard but in the real world it’s inflation, war, disease and climate – has arrived to collect the bill that is due.

Hunt is using the metaphor of Heart of Darkness as a reference to the colonial and neo-colonial exploitation of the rest of the world by the West. This was a theme in Putin’s most recent major address. Both Russia and China—but also much of the rest of the world—see themselves as seeking to break free from a system of colonial style economic exploitation and subjugation.

This is an Old Story.

I mean that the story of hubris at a societal level, where prideful human leaders lift themselves and their people up to unnatural heights by stealing what is not rightfully theirs, only to have their society struck down in retribution, is probably the oldest social narrative arc of them all. And that is exactly what our ... leaders have done in the United States over the past 25 years. In their overweening pride, they have stolen what is not rightfully theirs to lift themselves and their people up to unnatural heights. Through monetary and fiscal policies that have pulled forward future growth and productivity into the present, they have not only stolen wealth and prosperity from our children and our children’s children, but they have also created a political dynamic that has hollowed-out the Constitution and its attendant political norms.

We are a husk of ourselves. A wealthy and pampered husk of ourselves, but a husk nonetheless.

How did this happen? Here, I’ll show you.

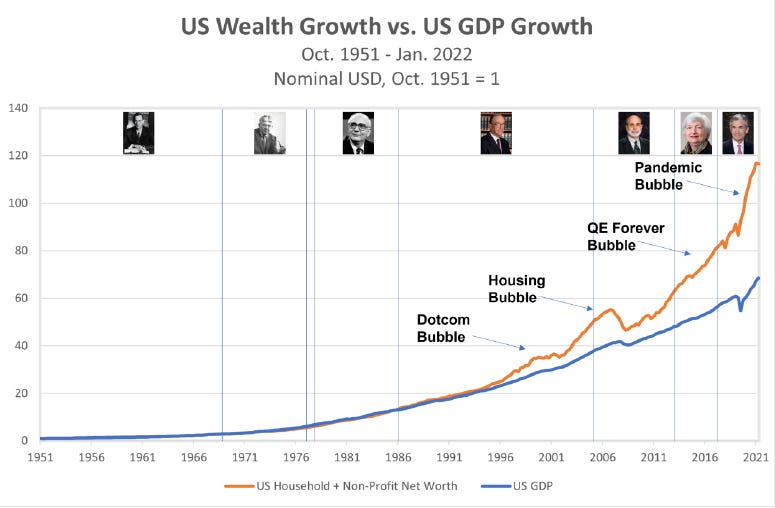

This is a 70-year time series of the growth in American wealth (US household and non-profit net worth) plotted against the growth in the American economy (US GDP).

As a people, you can’t be a lot richer than your economy grows without stealing that wealth from someone else.

Maybe it’s stolen from people in other countries through colonial terms of trade. Maybe it’s stolen from future people in your own country through artificially low interest rates, monetized debt-driven stimulus, and an increasingly levered financial system supporting increasingly non-productive mal-investment.

As you’d expect, the Nixon shocks in the early 1970s (ending the gold convertability of the dollar and punting the post-WWII Bretton Woods system) plus the OPEC oil shocks separated the absolute lock-step relationship between wealth growth and economic growth, but the two were still very much joined at the hip throughout the 1970s, ... US monetary policy over this period was consumed by trying to bring inflation down by any means necessary. As a result, it would have been inconceivable in the Volcker Fed (1979-1987) and the early days of the Greenspan Fed to even consider using monetary policy to inflate nominal wealth levels without risking resurgent inflation in the real economy.

By the mid-1990s, however, it was all too conceivable. About halfway through Alan Greenspan’s 20-year (!) Fed chairmanship, the Maestro had a revelation: blessed by the Great Moderation (high productivity and low inflation expectations), the Fed could use monetary policy as a political tool to make us richer than our economy could grow, without re-triggering wage/price inflation in the broader economy. By keeping interest rates lower than what would have been considered ‘normal’ over the prior few decades and by relaxing regulatory constraints on derivative securities, banking regulations and the like, Greenspan believed that he could inflate home prices and financial asset prices without hitting wages and prices more broadly.

Ben Bernanke was the first to double down on Greenspan’s epiphany, and he achieved that acceleration by expanding the instruments by which monetary policy could inflate financial assets directly. ... In simplest terms, QE just means buying enough stuff to drive the price of that stuff up and the yield of that stuff down. This has two big effects:

First, if you buy enough of something that’s a reference point for how all borrowing is priced, like US Treasuries, then artificially pushing the price up and the yield down should make all borrowing cheaper. This is the essence of pulling forward investment from the future. By making the price of borrowed money artificially lower, you encourage companies and households to borrow money today and buy something with it ...

Second, artificially pushing the price up and the yield down for something that is fundamental to every investment portfolio, like US Treasuries, means that all of the retirees and pension funds who buy US Treasuries and are counting on that yield as income to fund their retirement or their obligations are going to be forced to buy riskier assets, like mortgage-backed securities or dividend-paying stocks, to get that same level of income.

That situation – the worst Depression since the 1930s, where everyone is losing their job and no one is willing to invest any money in anything, and everyone is afraid that the entire financial system is about to collapse – is exactly what Ben Bernanke and the Fed faced in early 2009.

The problem – like it always is in this Old Story – was the transformation of emergency government intervention into permanent government policy.

The problem – like it always is in this Old Story – was the hubris of people like Ben Bernanke and Janet Yellen, who honestly believe that it is not only possible to rescue an economy through monetary policy, but that it is also then possible to control an economy through monetary policy. Yes, control. As direct market actions through more and more QE began to lose their edge as early as 2010, the Fed found yet another toolbox “to support a lagging economy”. They found narrative. They found that their words (‘forward guidance’ in the lingo, or sometimes ‘communication policy’) could be used instrumentally, not as a reflection of authentic belief or (god forbid) uncertainty and humility, but as a conscious tool to drive market behaviors in a desired direction. And that desired direction, of course, in the absence of inflation in the real economy, is always up.

The Yellen Fed was peak Fed. Peak, not in the sense of maximum balance sheet expansion, but in the sense of maximum faith and maximum zealotry that the Fed’s three toolboxes – short-term interest rates, balance sheet operations and communication policy – could achieve any desired macroeconomic outcome in this, the best of all possible worlds. Business cycle? What business cycle? Welcome to the era of permanent recovery! As for financial crises ... well, haha, it would perhaps be presumptuous to say that a financial crisis will never occur again, but with our current knowledge and tools for prudential monetary policy, certainly we can say that a financial crisis will not occur in our lifetimes. These were, in fact, Janet Yellen’s literal words. Ben Bernanke and Janet Yellen were true-believers in the power of monetary policy to control markets and the economy in a way that – in my experience as a former professional academic – only former professional academics can be.

I think that Jay Powell ... knows that it is economically unsustainable, socially destructive and politically poisonous to inflate wealth so much more than an economy grows.

I also think that Jay Powell, centimillionaire, has personally been an enormous beneficiary of the wealth-inflation policies that Alan Greenspan set in motion in the mid-1990s. I also think that Jay Powell, banker, would sooner betray his convictions than risk a tarnished reputation with his Wall Street tong as the man who ended the decades-long party.

And then came Covid.

And then came the economic response to Covid, which was not only a resumption of full-bore QE and balance sheet expansion (about $2 trillion worth), but also the largest stealing pulling forward of wealth for direct distribution to the already well-off of any government program in the history of man.

Again, I am 1,000% in favor of emergency government action to save an economy in general and to save jobs in particular. What our government did in reaction to the Covid recession and bear market was not that. ... More than 70% of the PPP distributions, more than half a trillion dollars, went to the richest 20% of American households.

For millions of Americans, particularly relatively wealthy Americans like lawyers and doctors and bankers and accountants and consultants and financial advisors, 2020 wasn’t a difficult year financially, it was their best year ever.

This is what broke the world.

How? Because the hundreds of billions of non-emergency dollars pulled forward from future Americans that went straight into the pockets of Americans who suffered zero economic damage from Covid on top of the hundreds of billions of non-emergency dollars pulled forward from future Americans that went straight into the pockets of relatively well-off Americans ... on top of the TRILLIONS of non-emergency dollars spent by the Fed to artificially lower the price of money and inflate financial assets and channel mal-investment and create the worst decade of productivity growth in the history of the United States and make us FEEL rich without BEING rich ...

Greenspan’s magic trick – inflating wealth without sparking inflation in the real economy – is dead. It doesn’t work anymore. There’s no more room for monetary policy to create “free” wealth, ...

Roughly speaking, we need a wealth destruction event that’s equivalent to the 2008-2009 Great Financial Crisis just to get the ratio of wealth to GDP back to pre-pandemic levels. If you sincerely want to eliminate inflationary pressure and expectations, that is.

Unfortunately, I think the political consequences of the wealth destruction now required to control inflation authentically ARE too unbearable for every status quo political institution, for both the Dems and the GOP. I think by far the most likely path forward is greater and greater political lashing-out into worse and worse policy positions, both economically and culturally.

Next up is economist Michael Hudson—talking about American Diplomacy. However, I think you’ll see that Hudson understands American Diplomacy to be driven, increasingly, by the type of flimflammery that Hunt described, and that leads—definitely in Hudson’s view—to a motive to re-colonialize the rest of the world. Sound excessive? Well, read on (in highly edited form).

Be aware that Hudson is an unabashed socialist who thinks that the Chinese have a fine and dandy system. That’s not me—I’m excerpting Hudson here for what I believe are his insights into the dynamics of American foreign policy and the dangers that it poses. Just as much as “democracy”, socialism devolves into oligarchy. Someone has to run things, right? The corruption of socialist ruling classes has been obvious at least since Milovan Djilas wrote The New Class. Ask yourselves, is Hudson’s description of American democracy as a “financial oligarchy” much different than Hunt’s view?

Once again, I have severely edited Hudson. What I’ve left is what I consider to be the most important core.

As in a Greek tragedy whose protagonist brings about precisely the fate that he has sought to avoid, the US/NATO confrontation with Russia in Ukraine is achieving just the opposite of America’s aim of preventing China, Russia and their allies from acting independently of U.S. control over their trade and investment policy.

Confronted with China’s industrial prosperity based on self-financed public investment in socialized markets, U.S. officials acknowledge that resolving this fight will take a number of decades to play out.

What is euphemized as U.S.-style democracy is a financial oligarchy privatizing basic infrastructure, health and education. The alternative is what President Biden calls autocracy, a hostile label for governments strong enough to block a global rent-seeking oligarchy from taking control.

Clausewitz popularized the axiom that war is an extension of national interests – mainly economic. The United States views its economic interest to lie in seeking to spread its neoliberal ideology globally. The evangelistic aim is to financialize and privatize economies by shifting planning away from national governments to a cosmopolitan financial sector. There would be little need for politics in such a world.

The U.S. drive to retain its unipolar power to impose “America First” financial, trade and military policies on the world involves an inherent hostility toward all countries seeking to follow their own national interests. ... The U.S. dream envisions a Chinese version of Boris Yeltsin replacing the nation’s Communist Party leadership and selling off its public domain to the highest bidder – presumably after a monetary crisis wipes out domestic purchasing power much as occurred in post-Soviet Russia, leaving the international financial community as buyers.

Russia and President Putin cannot be forgiven for having fought back against the Harvard Boys’ “reforms.” That is why U.S. officials planned how to create Russian economic disruption to (they hope) orchestrate a “color revolution” to recapture Russia for the world’s neoliberal camp. That is the character of the “democracy” and “free markets” being juxtaposed to the “autocracy” of state-subsidized growth.

...

The contradictory U.S. and European interests and burdens of the war in Ukraine

To return to Clausewitz’s view of war as an extension of national policy, U.S. national interests are diverging sharply from those of its NATO satellites.

The interruption of world energy, food and minerals supply chains and the resulting price inflation (providing an umbrella for monopoly rents by non-Russian suppliers) has imposed enormous economic strains on U.S. allies in Europe and the Global South. Yet the U.S. economy is benefiting from this, or at least specific sectors of the U.S. economy are benefiting. As Sergey Lavrov, pointed out in his above-cited press conference: “The European economy is impacted more than anything else. The stats show that 40 percent of the damage caused by sanctions is borne by the EU whereas the damage to the United States is less than 1 percent.” The dollar’s exchange rate has soared against the euro, which has plunged to parity with the dollar and looks set to fall further down toward the $0.80 that it was a generation ago. U.S. dominance over Europe is further strengthened by the trade sanctions against Russian oil and gas. The U.S. is an LNG exporter, U.S. companies control the world oil trade, and U.S. firms are the world’s major grain marketers and exporters now that Russia is excluded from many foreign markets.

... U.S. politicians support a bellicose foreign policy to promote arms factories that employ labor in their voting districts. And the neocons who dominate the State Department and CIA see the war as a means of asserting American dominance over the world economy, starting with its own NATO partners.

...

Russia has no discernable economic interest in mounting a new occupation of Central Europe. That would offer no gain to Russia, as its leaders realized when they dissolved the old Soviet Union.

Just as the Fed discovered “narrative”, so too have the Neocons. Propaganda is another name for narrative.

America’s foreign diplomacy no longer is based on offering mutual gain. ... today there is only the belligerent diplomacy of threatening to hurt nations whose socialist governments reject America’s neoliberal drive to privatize and sell off their natural resources and public infrastructure.

The first aim is to prevent Russia and China from helping each other.

Amazing as it may seem, U.S. strategists did not anticipate the obvious response by countries finding themselves together in the crosshairs of US/NATO military and economic threats.

The U.S. itself is ending the Dollar Standard of international finance

It is hard to see how driving countries out of the U.S. economic orbit serves long-term U.S. national interests. Dividing the world into two monetary blocs will limit Dollar Diplomacy to its NATO allies and satellites. ...

It is difficult to see how any diplomatic strategy can do more than play for time. That involves living in the short run, not the long run. Time seems to be on the side of Russia, China and the trade and investment alliances that they are negotiating to replace the neoliberal Western economic order.

America’s ultimate problem is its neoliberal post-industrial economy

The failure and blowbacks of U.S. diplomacy are the result of problems that go beyond diplomacy itself. The underlying problem is the West’s commitment to neoliberalism, financialization and privatization. Instead of government subsidy of basic living costs needed by labor, all social life is being made part of “the market” ... Income is obtained increasingly by financial and monopoly rent-seeking, and fortunes are made by debt-leveraged “capital” gains for stocks, bonds and real estate.

U.S. industrial companies have aimed more at “creating wealth” by increasing the price of their stocks by using over 90 percent of their profits for stock buybacks and dividend payouts instead of investing in new production facilities and hiring more labor. The result of slower capital investment is to dismantle and financially cannibalize corporate industry in order to produce financial gains. And to the extent that companies do employ labor and set up new production, it is done abroad where labor is cheaper.

...

The basic U.S. policy has been to threaten to destabilize countries and perhaps bomb them until they agree to adopt neoliberal policies and privatize their public domain. But taking on Russia, China and Iran is a much higher order of magnitude.

That leaves Western democracies with the ability to fight only one kind of war: atomic war – ... This is not diplomacy at all. ... But that is the only tactic that remains available to the United States and NATO Europe.

How then can the United States maintain its world dominance? It has deindustrialized and run up foreign official debt far beyond any foreseeable way to be paid. Meanwhile, its banks and bondholders are demanding that the Global South and other countries pay foreign dollar bondholders in the face of their own trade crisis resulting from the soaring energy and food prices caused by America’s anti-Russian and anti-China belligerence. This double standard is a basic internal contradiction that goes to the core of today’s neoliberal Western worldview.

This final paragraph is key to understanding the growing success of the BRICS movement. The US has flooded the world with debt—in the form of dollar inflation—that it has no intention of paying back. This is debt that was, in effect, imposed on the rest of the world. Now, as the US slides into crisis, the rest of the world is looking for a way out. Is the age of Western colonialism finally coming to an end?

"That leaves Western democracies with the ability to fight only one kind of war: atomic war – ... This is not diplomacy at all. ... But that is the only tactic that remains available to the United States and NATO Europe."

Perhaps not even that. We have not taken a nuclear weapon out of storage and tested it in a long time, and we no longer have the ability to produce tritium.

I don't have much use for hubris, nemesis, karma, or belief in a just world. America's leaders have, for generations, behaved as though the country had some bottomless strategic reserve to draw on in the event of trouble. In 1945 it did, but that was a long time ago. American leaders lack a skill that European statemen were once known for - the ability to maintain a balance of power among the Great Powers. That means both conserving your own strength and recognizing it's limitations. It also means the ability to work in cooperation with others, and not just dictating to vassals.

That was awfully long and it's a Saturday night here. For simple people like me it comes to simple things. We've borrowed from the future to pay for the now. When I say "we" I kind of me "they" because I never voted for any of it. A guy I listen to religiously says the simple part out loud, I paraphrase, "the laws of economics haven't gone away. They're out there, waiting to drop the hammer." This nation is hundreds of trillions of dollars in debt. When you take into account promises made by our cancerous federal gov't, we owe more than the entire world could produce for years. We are finacially doomed with no path to return to some sort of normal.

An analogy I heard once may be apropos - We went off the cliff sometime ago. We're just falling and don't know it. Sometime fairly soon we're gonna hit the bottom. When it happens we have a couple of scenarios - violence or we just simply fade away as a functioning nation-state. I don;t know which way is goes but I'm certainly no optimistic

"That leaves Western democracies with the ability to fight only one kind of war: atomic war – ... This is not diplomacy at all. ... But that is the only tactic that remains available to the United States and NATO Europe."

Perhaps not even that. We have not taken a nuclear weapon out of storage and tested it in a long time, and we no longer have the ability to produce tritium.

I don't have much use for hubris, nemesis, karma, or belief in a just world. America's leaders have, for generations, behaved as though the country had some bottomless strategic reserve to draw on in the event of trouble. In 1945 it did, but that was a long time ago. American leaders lack a skill that European statemen were once known for - the ability to maintain a balance of power among the Great Powers. That means both conserving your own strength and recognizing it's limitations. It also means the ability to work in cooperation with others, and not just dictating to vassals.

That was awfully long and it's a Saturday night here. For simple people like me it comes to simple things. We've borrowed from the future to pay for the now. When I say "we" I kind of me "they" because I never voted for any of it. A guy I listen to religiously says the simple part out loud, I paraphrase, "the laws of economics haven't gone away. They're out there, waiting to drop the hammer." This nation is hundreds of trillions of dollars in debt. When you take into account promises made by our cancerous federal gov't, we owe more than the entire world could produce for years. We are finacially doomed with no path to return to some sort of normal.

An analogy I heard once may be apropos - We went off the cliff sometime ago. We're just falling and don't know it. Sometime fairly soon we're gonna hit the bottom. When it happens we have a couple of scenarios - violence or we just simply fade away as a functioning nation-state. I don;t know which way is goes but I'm certainly no optimistic