Briefly Noted: Holy Moly Debt

Wolf Richter delivers the news that everyone with an IQ above room temp knew was coming:

There’s never a good time for this kind of news—as you’ll see from a few of the pictures below (not all included). Once the zero percent interest rate policy ended this was inevitable. It’s the blunt interest that the Fed uses to enforce fiscal discipline on politicians. Woops! Speaker Kev didn’t get the message.

Check it out:

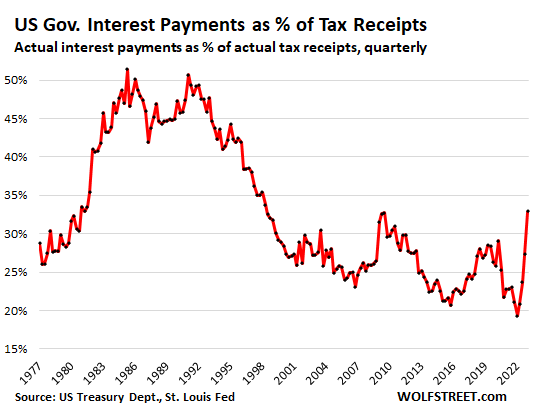

US government interest expense shot up over the past four quarters in line with higher interest rates and the ballooning pile of debt. At the same time, tax revenues fell from the peak levels in 2022 and are back where they’d been in Q4 2021, which had been a record high at the time.

So, interest expense as percent of tax revenues – the primary measure of the burden of the national debt on government finances – spiked ...

In the 1980s, interest expense as a percent of tax receipts was around 50%. In the decades since then, Congress has been footloose and fancy-free about its spending and taxing policies, and there hasn’t been any discipline, no matter who runs the show. It’s just that priorities shift. A high interest-expense burden might be the only discipline left that will put some common sense into these people in Washington.

Right, so in the 1980s when some of us were paying on mortgages at over 13% interest expense for the good ol’ government was correspondingly through the roof. Eventually something had to be done, and was.

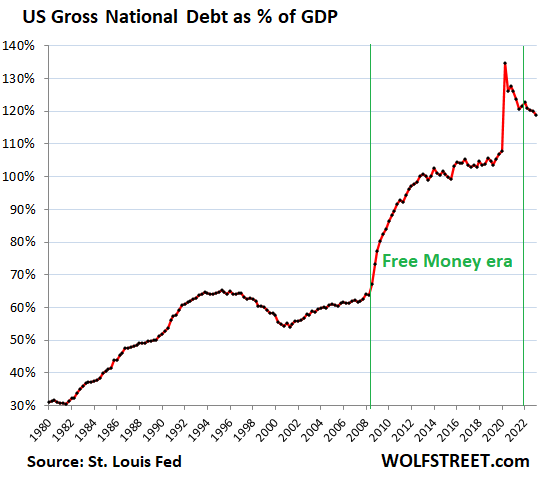

Here’s a picture that I really liked. Note that back in 1980 we still made stuff. The GDP was more meaningful back then, in my view. Now it seems to be more a measure of how well the rich are doing which each successive bubble that the taxpayers end up bailing out.

As I said, there’s never really a good time for those kinds of debt ratios, but this is coming at a particularly bad time. Speaker Kev wants to hand the Neocons a blank check to flush more money down the Ukraine drain—and we’ve been doing that at a phenomenal rate. Trust me on this one—we’ll never come out ahead on that one. Just as bad or worse, the rest of the world is no longer nearly as interested as they used to be in buying up US debt. In fact, some of the biggest holders are dumping US debt as discretely as possible, and some are even switching to gold. Correct me if I’m wrong, but this could foreshadow some serious inflation ahead.

Richter actually sees some good news—for the investing class. I don’t expect this to be great for the rest of us or for the country. Not without some change in spending:

Everyone knows that it was nuts to boost deficit spending as it was done over the past 5 years; it’s inflationary and contributed to the spike in inflation we have now; and as interest rates adjust to this higher for longer inflation, and as old securities with lower coupon interest mature and are replaced with new securities with higher coupon interest, the interest expense is going to be a headache.

On the other hand, fixed-income investors that buy those securities with the higher coupon interest are loving it, as they’re finally getting interest on Treasury bills that exceeds the current rate of CPI inflation. And those folks are going to pay federal income taxes on the interest income – along with folks who are paying income taxes on the interest income from CDs, money market funds, and high-yield savings accounts. So there’s more tax revenue heading toward the Treasury.

But what do I know. Comments are welcome.

Perfect summary. Just one thing left out. In 1929 there were many innovative technologies, business was booming, debt was low and we had gold in Fort Knox. 2023 and the economy is lousy, public and private debt are at all-time highs, people aren't working and stocks are in the stratosphere. There is an old saying. "Trees don't grow to the sky." What can't go on won't go on.

I was wondering when someone, anyone, would write an article about how much more it was going to cost the federal government to borrow money now that interest rates were rising. The free ride is over. While the politicians and news media try to scare people about the effects of a national default, the future holds another real dilemma fast approaching where just paying the interest on the debt is going to inevitably reduce budgets and borrowing by the government. As Victor Davis Hanson wrote in a column recently - not about this topic - but it fits: What can't go on won't go on.