Banking And Money Roundup--Gold, Re-Mercantilizing The Global Economy, Etc.

Many readers will have seen/heard Sen. John Kennedy’s remark about banks and banking. For those who haven’t, Kennedy basically said that a banking system is dependent on trust and that banks are run as “sophisticated Ponzi schemes. Whether or not you consider that an entirely fair or accurate characterization, what is true is that banking does fundamentally involve risk taking—part of the cost of receiving a loan from a bank will involve covering the bank’s inevitable losses on loans that go bad. All loans involve some degree of risk. Ideally, the risks are calculated risks and the good loans will more than cover for losses. The systemic problem arises when calculation of risk in the banking sector is replaced by exuberant optimism or, nowadays, the expectation that a third party—the government in some shape or form—will bail the banks out. The financial sector in the US is far more complex than just banks, but the basic ideas underlying the banking sector are similar in principle to most business activity. The difference lies in the key role played by banks in facilitating business activity as well as the lives of ordinary citizens.

Currently there are two somewhat related concerns in financial circles. One is the continuation of King Dollar as the world’s hegemonic reserve currency—under attack by countries outside the collective West, led by Russia and China but including an increasing number of significant nations. Uncertainties on that score, fueled by the economic uncertainties caused by the backfire of the Sanctions War on Russia, have also played a part in concerns of a looming recession and of a looming financial crisis. Also involved in all this—and I’m not the one to apportion the role of each factor—is the ongoing struggle of the Jay Powell led Fed to wrest control of US monetary policy from the global financial elites that Tom Luongo refers to as “Davos”. That struggle has featured Powell’s Fed raising interest rates drastically, from the zero bound that they’ve been set at for years—free money for the financial elites that has led to radical misallocation of capital in the Western economies.

Today I came across a collection of articles bearing on multiple aspects of this crisis, so a roundup seems a good idea. Many, although not all, of these articles were picked up from Zerohedge.

First, there’s an interesting article by a Spanish “economist and fund manager”, Daniel Lacalle. Lacalle discusses and compares the risks facing the banking systems in the US and in Europe, and he does so in a way that I found to be fairly accessible. One of his key points is one that we’ve mentioned in the past: In the “real economy” of the US banks, per se, only provide about 20% of the financing—the rest comes through the issuance of corporate bonds and other types of financing. In Europe, on the other hand, 80% of the “real economy” is financed through bank loans. We’ll return to that, because it has a bearing on the overall economic risk involved in the respective economies going forward.

European banks may be riskier than U.S. ones and regulation will not solve it.

Lacalle begins by pointing to a symptom of excessive risk taking in the US banking system. Deposits at commercial banks have fallen to a two year low, while banking credit is at a new high: $17 trillion. Lacalle sees this continued credit expansion as dangerous, resting on expectations of the Powell Fed “pivoting” back to easy money:

The inevitable credit crunch is only postponed by a consensus view that the Fed will inject all the liquidity required and that rate cuts will come [down] soon. It is an extremely dangerous bet. Bankers are deciding to take more risk expecting the Fed to return to a loose monetary policy soon and expecting higher net income margins due to rising rates despite the elevated risk of increasing non-performing loans.

Worse, perhaps, is that this excess is coming at the end of years of similar excess that have resulted in systemic instability and risk:

The banking system collapses are symptoms of a much larger problem: Years of negative real rates and expansionary monetary policy that have created numerous bubbles. The risk in the banks’ balance sheet is not just on diminishing deposits on the liability side, but a declining valuation of the profitable and investment part of the assets.

He maintains that the level of debt is now so high that few banks will be able to raise equity when the “inevitable crunch” comes. The question that arises in my mind is: Given that US banks only finance 20% of the “real economy”, is that diversification of the risk a plus for the US economy? How solid are corporate loans, etc.? Lacalle doesn’t address that directly, but instead pivots to Europe. Having first noted that European banks were much slower in recovering from the crisis of 2008 than were US banks, he describes the hidden risks in the European system.

On paper, the European banks appear to have strengthened their balance sheets since 2008, but in reality the underlying capital is weaker than it looks. What he then describes appears to me to relate directly to the sanctions backfire and resulting economic and financial distress in Europe—governments and large corporations are under financial pressure that they did not—probably could not—foresee and for which there are no obvious short term remedies. Rapidly rising interest rates and rapidly rising energy costs with all the rippling effects throughout their economies:

European banks lend massively to governments, public companies, and large conglomerates. The contagion effect of a rising concern about sovereign risk is immediate. Additionally, many of these large conglomerates are zombie firms that cannot cover their interest expenses with operating profit. In periods of monetary excess, these loans seem extremely attractive and negligible risk, but any decline in confidence in sovereigns can rapidly deteriorate the asset side of the financial system rapidly.

...

What does this mean? That the biggest risk for European banks is not deposit flight or investment in tech companies. It is the direct and uncovered connection to sovereign risk. …

Lacalle discusses all of this in further detail, but concludes with this warning of what may be coming to Europe:

The combination of ignorance and arrogance led Europeans to believe they were immune to the 2008 crisis because they believed in the miraculous power of their bureaucratic and bloated regulation. No amount of regulation helps when the rules are all designed to allow rising exposure to almost-insolvent governments under the excuse that it requires zero capital and has no risk. Sovereign risk is the worst risk of all. European banks should not fall into the trap of thinking that tons of rules will eliminate the risk of a financial system crisis.

Now we do a pivot to larger economic and monetary developments.

First we have a lucid discussion of the prospects for the BRICS coalition to topple King Dollar as world reserve currency:

Why China & Its Trading Allies Are Well Placed To Topple The U.S. Dollar

New Statesman ^ | 05/07/2023 | Wolfgang MunchauAfter decades meting out sanctions and financial coercion, the US may soon feel its grip on world trade beginning to loosen...

“Soon” is, of course, a relative term. A major point of this article is that changing basic paradigms—such as a world monetary and economic system—is difficult and takes time. The author’s argument is that the US weaponisation of King Dollar, through the use of sanctions, has pushed matters to the breaking point. As Sen. Kennedy said about banks, these matters ultimately rest on trust, and that’s the capital that the US Neocon led foreign policy elite have wantonly destroyed. But it’s still not as simple as simply wanting to change:

Brazil, Russia, India, China and South Africa. Their economic-development models have succeeded but have also critically depended on the US dollar. ... The willingness of the US to absorb the world’s savings surpluses was the engine of globalisation. It ensured that the dollar would maintain its status as the world’s leading currency.

...

If the five Brics countries wanted to end their dependence on the dollar, they would have to do more than just choose another currency to trade in. … [They] would have to change how they interact with the rest of the world, and with one another.

…

Changing economic models is hard. ... All of this would take a long time – one or two decades, perhaps.

The author provides detailed argumentation for these views, but in the end believes that US abuse of the privileges of King Dollar has brought about the will to find a way. That there is movement in the direction of less reliance on the dollar and toward other alternatives is clear enough from this chart:

Of course, this transition won’t happen overnight. As an example, we know that India has been buying vast amounts of Russian oil and reselling it to the EU at a steep markup. India has been paying Russia in rupees, but Russia is now looking to have India pay in other currencies, too—presumably the Euros India has been accumulating. Russia simply doesn’t have a use for the amount of rupees it now has. So, what we’re probably seeing is a new era of monetary flexibility on the international scene. The dollar’s role has been steadily but gradually decling for decades. It may now accelerate while still retaining a role commensurate with the US place in the world economy. A bigger question may surround the Euro.

Michael Every of Rabobank pushes back at the notion of dedollarization—to an extent. He uses the example of the rupee and the ruble, as I just did. However, he points, as I did, to a more “diverse” global monetary regime. One in which the dollar retains an important role, but not as dominant as it was. In place of that globalist regime, which had the dollar at its core, Every predicts the return of mercantilism:

The Neoliberal Globalization King Is Dead! Long Live The Mercantilist Industrial Policy King!

That’s before we get to dedollarisation. Last week’s news that INR-RUB bilateral trade isn’t working because Russia doesn’t want to hold INR laughs at dollar bears. Yet it also shows the two countries must shift their physical trade patterns to match desired FX holdings, or bring in another economy and use that FX instead, which is all being pondered. Wolfgang Munchau argues ‘Why China and its trading allies are well placed to topple the dollar’: yes, if they want to embrace global disorder. Dedollarisation it’s not something that will happen via a flick of a switch - but it might do via the press of a button. To push back, the US would need to keep rates (and defence spending) higher for longer. Yet that creates global dollar shortages, more so as commodity prices now move with, not against the dollar. So, that requires Fed swaplines to EM, not just DM. But no US swaplines are going to head to China and Russia. As such, destabilisation --and more contagious global mercantilism-- surely lies ahead. As does a stronger dollar, which remains king even as many plot to behead it. As they say, if you aim to shoot the king, you better not miss.

To conclude: The neoliberal globalisation king is dead! Long live the mercantilist industrial policy king!

The problem with Every’s predictions, I would argue, is that they fail to take into account the many moving parts in this scheme and the amount of time that this shift will take. We can accept, with Tom Luongo that King Dollar won’t be replaced in the near future, but replacement is not required to effect change in economic dynamics, at home and abroad:

@TFL1728

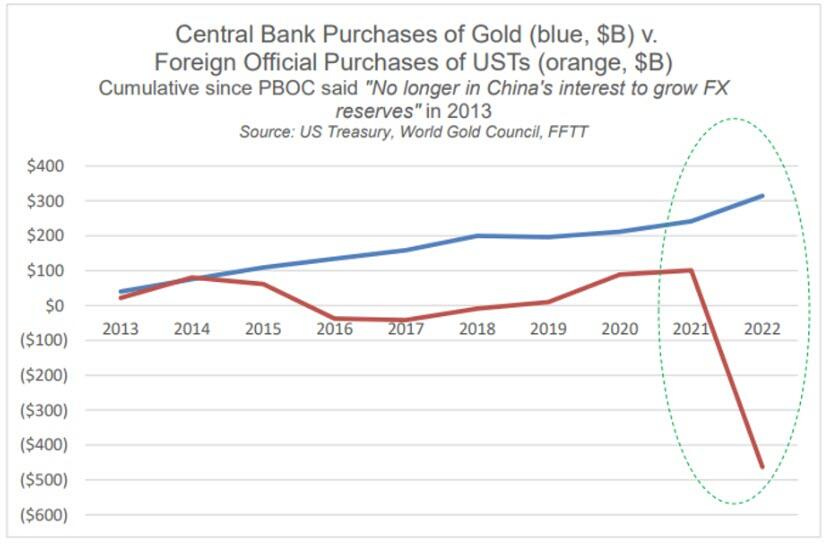

Central Bank's continue buying gold to build reserves. The buying began in 2010 and has accelerated in the last 3 q's.

Why? The world went to ZIRP, Europe went to NIRP and those leading the charge (Russia & China) are aligned to offer a competitor to the USD. /1

That competitor, however, is years off, not months.

When China restates its reserves to 20+% of their M2 I'll consider it. Russia is buying [gold] again as the Ruble internationalizes within the oil trade. /2

As proof of a US turn towards re-industrialization Every cites the Jake Sullivan speech that we took apart just yesterday. But, as we saw, that speech was as much about the US War On Household Appliances as it was about any credible and serious turn to re-industrialization. Every also points to plans for more defense spending within the US, but US government spending—including defense spending—is running up against the very real limits of our sovereign debt. Those limits are going to be greatly exacerbated by the declining stature of the dollar—that is a process that started decades ago and is simply gaining momentum. No, the dollar won’t be dethroned tomorrow, but the effects of the changing monetary regime will be felt—are already being felt. And re-industrialization on the scale needed will not happen in just a year or two, just as deindustrialization didn’t happen overnight. And reindustrialization will not be a simple process that will happen without financial, budgetary, political, and social destabilization.

https://www.lifesitenews.com/news/jp-morgan-chase-persistently-discriminated-against-conservatives-19-republican-ags/

When I worked in the industry 10 years ago, European banks were nowhere near as strong as US banks.

One problem the Europeans have is there are only a handful of banks per country. The government may even hold a significant stake in the bank - known as the golden share. It's hard for a government to make its banks charge off problem loans when the government is a major shareholder.